Share

The Capability and Innovation Fund offers a unique window of opportunity. Fintechs should seize it

There’s no time like the present in the UK Small Business Banking sector.

There’s no time like the present in the UK Small Business Banking sector.

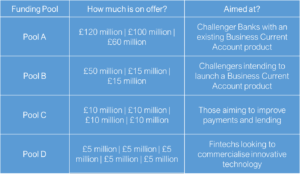

There is £425 million of funding available for focussed Banks and Fintechs through the RBS-funded remedy package (born out of the UK govt. bailout of RBS back in 2008).

Of this, £65 million could be argued to have been directly earmarked for the most innovative in the UK Banking sector, namely Fintechs (through Pools C and D).

The remaining £360 million is split between two pools with criteria aimed at Challenger Banks who have or have announced they will launch Business Current Accounts.

Since the initial appointments of industry experts to the body administering the funds (BCR), there have been a number of delays. In hindsight, this should have been expected – The Capability and Innovation Fund represents a large amount of (mostly) taxpayer money that must be carefully administered to achieve better outcomes for UK SMEs.

The delays themselves are to the opening of the application process for Pool A onwards, along with the announcement of winning applications. Better news for those Banks waiting to pull the trigger is that there will be an official meeting for eligible applicants to Pools A-C in late September, with the application process for Pool D still under consideration. Pools A to C are due to occur sequentially according to government material found on gov.uk.

In addition to a delay, hopeful Challengers have been faced by a market-shifting event, the merger of CYBG and Virgin Money. CYBG will gain scale via 3.3m customers in the mortgage market and expand into credit cards. Virgin Money will gain access to 2.8m current accounts and small business lending.

Challenger Banks and Fintechs can help their own causes through positive partnerships and PR associated with making an application. Partnerships in this space are not new, but the increase in the pace suggests a change in core strategy. A clear example occurred in late 2017, when CYBG´s CEO, David Duffy, called for the adoption of an ecosystem approach within CYBG in an investor call, where maximising ease of co-operation (‘making the pie bigger’) with Fintechs and other service providers became the name of the game. CYGB has reportedly already invested £5 million on their application to the Capability and Innovation fund.

Other trailblazing Challengers such as Tide, Starling, Monzo and Revolut are eye-catching not simply for their sleek UIs and cool functionality, but the number of partnerships they strike to maximise ease of use and utility. Other Challengers will need to up their own collaboration with Fintechs to follow suit.

How can Fintechs maximise the value of applying to the Capability and Innovation Fund?

Due to the delay and pending merger, all Challengers are likely to now assess and augment their original applications.

Fintechs should therefore make the most of the unique circumstances that surround the Capability and Innovation Fund to drive a collaborative approach with Challenger Banks. The Fund is ultimately aimed at improving SME outcomes. Many Fintechs do this already, but many more are capable of doing so and offer services that meet the criteria to make an application.

Announcing an intent to bid may well highlight their own pursuit of innovation in addition to making it clear to Challenger Banks that your firm may be interested in partnering.

Whilst applicants do not need to meet criteria such as having a Banking license to apply for Pools C and D, there are a number of criteria for eligible bodies (link to updated criteria issued on the 2nd of May here). Most importantly (respectively) for Pools C and D are:

“offers, or has expressed an intention to expand its business offering to include, lending or payment services to SMEs in the United Kingdom or international payments services to SMEs in the United Kingdom”

And

“which (a) provides or develops financial products or services predominantly to or for SMEs in the United Kingdom or (b) provides products or services to the businesses described in (a) ”Pools C and D encompass the vast majority of eligible Fintechs, but this does not rule out a means of growing their business and delivering better outcomes from Pools A and B.

This is where the delay and CYBG/Virgin Money merger comes in:

All Challenger Banks are now likely to be seeking out means of augmenting their own proposals to deliver better outcomes to SMEs. Fintechs therefore need not solely apply to pools they are eligible for but could approach Challengers to assess whether there is another potential fit. This has a double benefit of Banks securing innovations sooner that they would have previously, with Fintechs being able to enhance sooner as a result.

While the prospect of winning a sizeable level of funding or partnerships with Challengers are considerable rewards in themselves, there are additional benefits that will ensure Fintech’s that apply end the process in a better shape than when they started.

These include the business plan that forms part of a submission, a planned roadmap of technology and service development, in addition to mapping out a strategy for commercial growth.

Fintechs that are looking to grow have a unique window of time in which they could benefit from not only the potential funding on offer, but also the fact the Capability and Innovation Fund arguably takes incentives to co-operate a step further. By potentially removing the costs of co-operation within a limited time frame, UK Fintechs and Challenger Banks could establish new ways of working that help ensure positive SME outcomes to compete with the ‘Big 4’ Banks.

UK Banking has evolved substantially in the previous decade, with fears of competition from Fintechs transforming into an improved understanding and a desire to increase levels of cooperative engagement. They are now seen more as potential partners than as a threat to banks´ existence.

Axis is holding an event in October to discuss the application process for Pools A-C, which will make sense of the process set out and provide further insight on how to capitalise on this unique funding opportunity.

Axis Corporate is a Financial Services focussed management consultancy, with a track record of working with Fintechs and Banks in the UK, US and Spain.

Related article on The Capability and Innovation fund

The Capability and Innovation fund will change the SME Banking market. Is your Bank ready?